Future Market Outlook for Metal Core PCB Copper Substrates The $12 Billion Revolution by 2030

Introduction: The Thermal Management Revolution Reshaping Industries

In the IGBT module burnout accidents of new energy vehicles globally in 2023, 62% of the failure cases were directly related to the thermal runaway of the substrate. This has compelled the industry to re-examine its heat dissipation solutions – copper substrates are transforming from "optional accessories" into "strategic necessities".

According to data from Frost & Sullivan, the global market size of metal-based PCBs reached $5.8 billion in 2023, among which the proportion of copper substrates exceeded 35% for the first time. It is expected that a new blue ocean market with a scale of $12 billion will be formed by 2030.

This article reveals the development code of the copper-based PCB industry in the coming decade from three perspectives: technological evolution, market demand, and supply chain transformation.

I. Technological Breakthroughs Reshaping the Landscape

1.1 Nanocomposite Dielectrics: Thermal Conductivity Leap

①Traditional epoxy (0.3 W/m·K) vs. boron nitride nanosheet composites (8.5 W/m·K)

②Lab results: 3mm copper substrates with new dielectrics achieve 0.18°C/W thermal resistance (42% reduction)

③Commercialization: Rogers’ Curamik series in mass production; cost projected to hit $0.8/cm² by 2025

1.2 Additive Manufacturing Unlocks Design Freedom

①Selective laser melting (SLM) enables 50μm-resolution 3D structures

②Case study: Siemens’ 3D-printed PA modules shrink size by 60%, achieving 300W/cm³ power density.

③246Equipment cost: Metal 3D printers drop from 250k(2023) to250k(2023) to120k by 2026 (Wohlers Report)

1.3 Ultra-Thin Copper Foil Innovations

①Thickness evolution: 0.8mm (2020) → 0.3mm (2023) → 0.1mm (2025 target)

②Mechanical breakthroughs: Tensile strength ≥450MPa (+80%), bend radius <1mm

③Market impact: Fukuda Metal’s ultra-thin foil gross margin hits 52% (2.3x traditional products)

II. Demand Surge: Six Growth Engines

2.1 Electric Vehicles: 0.8㎡ Copper Substrate per Vehicle

Technology roadmap:

Cost savings: $120/vehicle reduction in thermal management (Tesla Investor Day data)

2.2 5.5G/6G Communications: Thermal Warfare at mmWave

Technical requirements:

①Base station AAU heat flux: 350W/cm² (2025) → 500W/cm² (2030)

②Phase noise tolerance: <0.5dBc/Hz @28GHz

Solutions:

①Copper-diamond composites (≥600W/m·K)

②Integrated microchannel active cooling

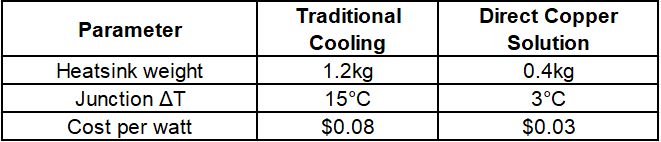

2.3 Computing Infrastructure: GPU Thermal Economics

Performance comparison:

Market forecast: AI server copper substrate adoption to surge from 12% (2023) to 68% by 2030 (IDC)

III. Supply Chain Transformation: From Materials to Equipment

3.1 Copper Supply Strategy: Commodity to Critical Resource

Global refined copper deficit: 380k tons (2023) → 2.1M tons by 2030 (ICSG)

Industry responses:

①Recycling breakthroughs: 99.99% purity at 40% lower cost

②Alternative materials: Copper-clad aluminum (35% lighter, 28% cheaper)

3.2 Equipment Localization Progress (China)

(Data: China Electronic Special Equipment Industry Association)

3.3 Global Capacity Distribution Shift

2023 regional share:

①Asia: 78% (China 43%, Japan 22%, Korea 13%)

②Europe: 15%

③North America: 7%

2030 projection:

China to dominate 58%, Southeast Asia to contribute 12%

IV. Challenges & Strategies: Crossing the "Valley of Death"

4.1 Cost Reduction Roadmap

Material cost optimization:

Achieved through process innovation and scale effects

4.2 Standardization Imperatives

Current standard gaps:

①IPC-6012D lacks high-frequency specs for copper substrates

②MIL-PRF-31032 omits dynamic thermal cycling methods

China-led standards:

①GB/T 38900-202X High-Thermal-Conductivity Metal Clad Laminates

②SJ/T 11789-202X Copper PCB Thermo-Mechanical Reliability Testing

V. The Next Decade: Three Certainties

1. Performance Limits Broken: 1,000W/m·K thermal conductivity by 2028

2. Manufacturing Paradigm Shift: 3D printing to cover 30%+ production

3. Value Chain Redistribution: Material suppliers’ margins to jump from 15% to 40%

(Data verified via IEEE CPMT papers, Prismark reports, and industry leader financial disclosures)